| AFRICA & MAURITIUSStructured Products And Derivatives Association |

|

| AFRICA & MAURITIUSStructured Products And Derivatives Association |

The AMSPDA Risk Ratings are designed to:

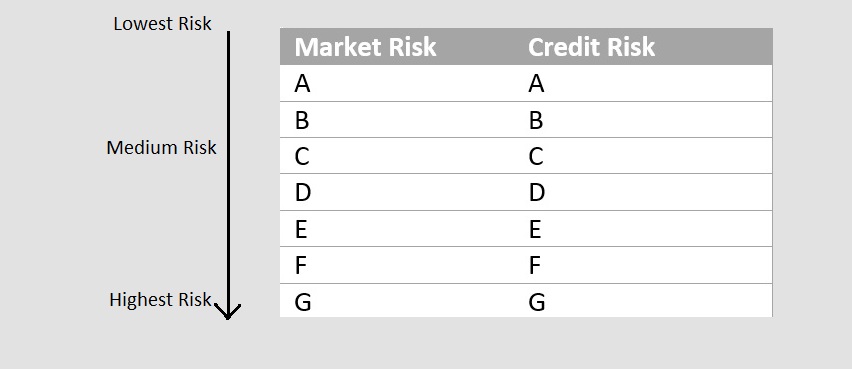

The AMSPDA put together for investors a chart which will give an overview of market risk and credit risk associated to a particular product.

The chart combines market exposure and credit exposure of a particular product to outline the overall risk associated to a product.

Investors in structured products typically face two main risks:

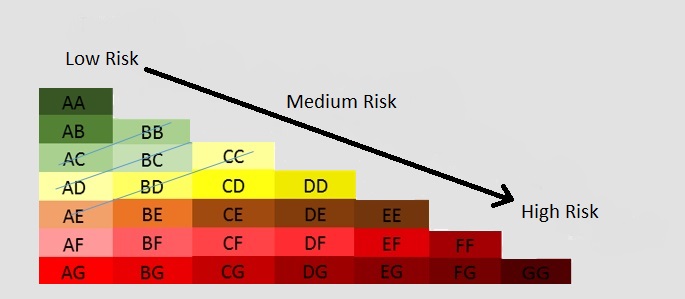

For instance, if a product scored BF, that product includes low levels of market risk, but high levels of counterparty risk.

Similarly, a product scored at AC includes lowest levels of market risk, but medium level of counterparty risk. The objectives have been designed to satisfy a set of objectives, in line with the objectives of certain international bodies, including the Committee of European Securities Regulators (CESR).

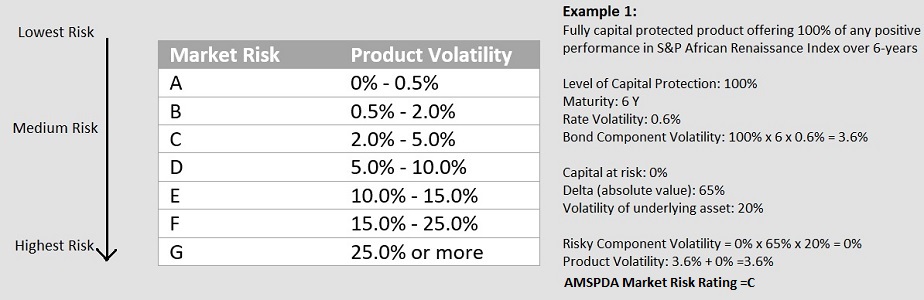

Market risk is generally based on the volatility of a product. Considered as an essential measure of risk, volatility assess how much uncertainty there is about the future value of a security. Calculating the volatility entails into breaking up the product’s components:

The bond part is actually the risk free side of the product which also caters for any capital protection at maturity. The level of capital protection offered at maturity, if any, determines the risk profile of a product, as it eliminates the possibility of losing capital if the underlying asset does not perform as expected. Volatility of this component is based on the volatility for the rate implied for the corresponding Zero Coupon Bond, multiplied by the term of that bond.

Ideally, structured products are designed to offer exposure to a particular underlying asset. ‘Delta’ determines the level of exposure to the underlying asset. Therefore, high delta products will offer high exposure to the underlying and low delta products will offer low exposure to the underlying.

The volatility of the risky component also depends of the volatility of the underlying asset. Typically, a fair measure will be the 5-year realized volatility of the underlying asset, readily available on Bloomberg or Reuters.

Risky Component Volatility = Capital at Risk x Delta x Volatility of underlying asset

For a fully capital protected product, the risky component does not contribute at all to the volatility of the product as there is no capital at risk.

Therefore, if we had a set a general method of calculation for the product volatility, it would be as follows:

Product Volatility = Bond Component Vol (Capital Protected x maturity x rate volatility) + Risky Component Vol (capital at risk x delta x volatility of the underlying asset)

The AMSPDA Credit Rating is determined based on the credit rating assigned to the issuer of the structured product. Although the cash flows of a structured product are derived from other sources, the product themselves are legally considered to be the issuing financial institution’s liabilities. On the other hand, for deposit-based plans, it will be the risk of default of the deposit taker.

Below is a chart put together for ease of reference:

Collateralized product will bear the same credit ratings of the issuer for the collateral. For instance, if the product is collateralized by a sovereign bond, the credit rating will be that of the issuing government / state.